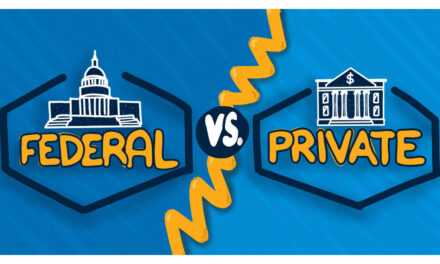

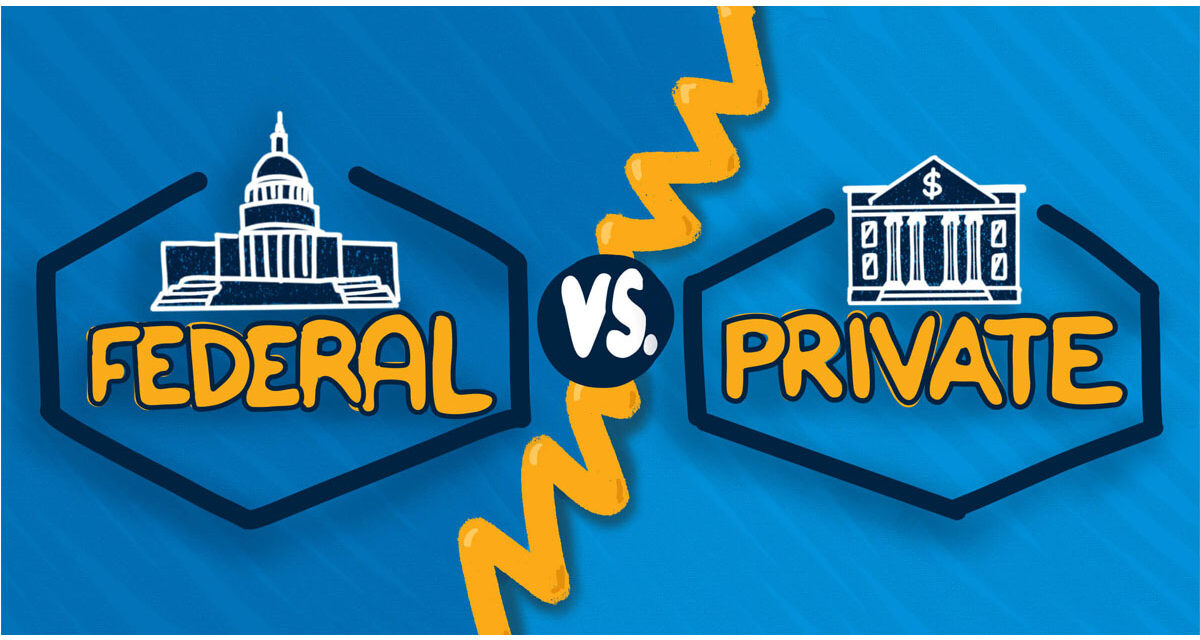

Cato Institute: The Case for Privatizing Student Loans

America’s student loan system is deeply flawed, and now may be the best time in decades to fix it. According to a recent policy paper from the Cato Institute, the federal government’s involvement in student lending has created costly problems for students, taxpayers, and colleges. The paper, written by research fellow Andrew Gillen, argues that the federal government should get out of the student loan business and turn it over to private lenders. Cato believes this change would save money, reduce risky borrowing, and improve outcomes for students. “The stars have aligned,” Gillen writes, “to present the best chance in decades of ending the federal government’s student lending and replacing it with a system that harnesses the advantages of a marketplace of private lending.”

This article looks at what’s wrong with the current system, how privatizing student loans could work, and how such a change would impact students, colleges, and the broader economy.

What’s Wrong with the Current Student Loan System?

The federal student loan system was created to help students pay for college, but it has turned into a program with growing financial losses and unintended consequences. Currently, the government lends directly to students through programs managed by the Department of Education. These loans are given out with the same interest rate and terms, regardless of the student’s background, academic performance, or chosen major.

But this approach has led to a flood of loans for programs that offer little to no return on investment. “Preston Cooper estimates that around 31 percent of students attend a program with a negative return on investment,” the Cato paper explains. In other words, nearly a third of students borrow money for degrees that leave them worse off financially. Some programs have even been found to have returns as low as negative 32 percent, according to Nobel Prize-winning economist James Heckman and his coauthors.

The government continues to fund these risky educational choices, but it is students and taxpayers who end up paying the price. Students are left with debt they struggle to repay, and taxpayers are on the hook for loans that are never fully paid back.

Meanwhile, colleges have little reason to care whether students succeed. “When a student defaults on a loan,” Gillen writes, “both the student and the government are harmed… But the college still benefits since it is paid up-front and gets to keep all the money.” This creates a system where colleges are rewarded even when they fail to deliver a valuable education.

The scale of the problem is massive. According to the Education Data Initiative, the federal student loan portfolio is now worth about $1.7 trillion. Yet recent changes in loan forgiveness policies have made this system even more costly for the government.

In 2019, the government believed it was making a profit of 5 cents for every dollar it lent. But after President Biden’s administration introduced new forgiveness plans and more generous repayment terms, those projections flipped. Now, the government expects to lose 19 cents for every dollar lent. These losses are partly due to the Saving on a Valuable Education (SAVE) Plan, which increased the income exemption and reduced monthly repayment amounts for many borrowers.

Cato estimates that ending all federal student lending would save the government about $212 billion over the next 10 years. Gillen explains: “Over the next 10 years, there will be $1.1 trillion in new student loans, and the government is projected to lose an average of $0.19 for each dollar lent. Thus, eliminating all federal loan programs would save the government $212 billion.”

How Could a Privatized System Work?

Privatizing student loans would mean ending federal loan programs and allowing private lenders to offer student loans directly. These lenders would compete in the market, and students would choose the best options available. The loans would still help students pay for college, but the money would come from private institutions, not the government.

There are two main ways to make this change. One option is to completely stop new federal student loans. The second option would keep the Direct Loan program’s structure in place but switch from government funding to private capital. In this second model, the Department of Education could oversee a marketplace where lenders compete to offer loans to students, similar to how insurance plans are offered on healthcare exchanges.

Gillen emphasizes the need to move quickly. If the courts overturn Biden’s repayment plans, or if a future Trump administration rescinds them, the expected savings could disappear. “If courts throw out the rest of the Biden administration’s changes to student loans, or if the Trump administration rescinds them… much of the savings will disappear,” he warns. “The best chance to get the government out of the student loan business in decades will be lost.”

What Would Change for Students?

In a privatized system, students would still be able to borrow money for college, but the process would be very different. Unlike federal loans, where every student receives the same interest rate, private lenders would set rates based on risk. A student attending a high-quality college and studying a major with strong job prospects would likely receive a lower interest rate. On the other hand, a student going to a low-performing college for a degree in a field with few job opportunities would be seen as riskier and might face higher rates—or may not qualify for a loan at all.

This type of system would give students clearer signals about the value of their educational choices. “Interest rates can convey useful information,” Gillen explains. “The vast differences in risk of these students’ college paths would be accounted for by lower interest rates for the less risky path.” In other words, the price of borrowing would reflect the actual value and risk of the education being pursued.

Private lenders would also reward students who perform well academically. Gillen points out that “students would have an incentive to work hard in school since lenders would offer lower interest rates to students with good grades and high test scores.”

How Would Colleges Be Affected?

For colleges, a shift to private lending would bring new accountability. Right now, colleges are paid upfront with no consequences if their graduates struggle financially. Private lenders, however, would track repayment outcomes and steer students away from schools that consistently produce poor results.

Colleges that want to attract more students would need to improve their graduation rates, job placement services, and overall quality. If their students repay their loans successfully, lenders will offer better loan terms, making that college more attractive. As Gillen puts it, “Colleges would be rewarded for improving.”

This change would push schools to deliver real value. It would no longer be enough to simply enroll students and collect tuition. Colleges would have to prove that their programs lead to success after graduation.

What Are the Arguments in Favor?

Supporters of privatization argue that a market-based system would fix many of the problems caused by federal lending. One major benefit is the reduction of malinvestment. Private lenders would not issue loans to students unlikely to succeed because they would lose money if those loans are not repaid. This natural filter would prevent thousands of students from borrowing for degrees that offer no economic benefit.

Another argument is improved accountability. In the private system, colleges would need to earn their funding by producing successful graduates, not just by enrolling as many students as possible. Students would also make more thoughtful decisions if interest rates reflected the real risk of their educational choices.

Gillen lists five major advantages of private lending: fewer bad investments, more accountability for colleges, better incentives for students, better incentives for colleges, and more informed decision-making.

What Are Critics Saying?

Critics of privatization raise concerns about access and fairness. They argue that private lenders may avoid giving loans to students from low-income backgrounds or those with lower grades, which could make college less accessible to some. There is also concern that lenders would favor students in fields with high salaries, such as engineering or finance, while students in the arts or public service might be left behind.

Some experts warn about possible abuse. Without strong regulation, private lenders could impose harsh terms or exploit students who don’t fully understand loan agreements. Others fear that shifting the system to private hands could create confusion and chaos, especially during the transition.

There is also uncertainty about who would manage student loans if the Department of Education is dismantled. President Trump has said he wants to close the department and move student loans to another agency, possibly the Treasury Department or the Small Business Administration. But as Gillen notes, “The SBA would be a strange choice,” since it was built to process small business loans, not manage the debts of more than 40 million student borrowers.

Critics also argue that dismantling the Department of Education could harm other essential functions like Pell Grants, civil rights enforcement in schools, and funding for students with disabilities.

A Chance to Act

Despite the concerns, advocates for privatization say the time to act is now. Government loans are no longer profitable, and continuing down the same path could cost taxpayers hundreds of billions of dollars. If Congress moves quickly, it could save money and begin building a better system that rewards student success and holds colleges accountable.

But this opportunity may be short-lived. If courts strike down Biden’s forgiveness plans, or if a new administration reverses them, the savings that make privatization politically possible could vanish.

As Gillen puts it, “Congress will need to move quickly to seize this opportunity.” If lawmakers act, they could reshape the future of higher education financing in a way that protects students, strengthens colleges, and saves taxpayers billions.

PB Editor: One thing that is not covered here is that government sponsored loans take on a socialist flavor which pushes pricing higher and higher. As Reagan said, “whatever you subsidize, you get more of.” And what we are subsidizing is higher tuition, so we continue to get more inflation in university costs.

{kind=link}

Larry, Economics is what you received your bachelors degree studying back in the 60's. Adam Smith's laws of economics has…

A foreign country isn't giving you money with no strings attached. Even American donations would hardly be neutral. FARA should…

Seth, I understand. The passage had numbers and a few big words. Let me know what you need clarification on.

Should have said 1.5 years not 2.5 years

Trump said tariffs will not raise prices and Seth believed. Trump said he would bring prices down on day one…